Q3 2015 Review & Comment: Keeping Frankenstein on the Table

“This is a monetary moment. I think we are looking at the beginning of the world’s reappraisal of the words and deeds of central bankers like Janet Yellen and Mario Draghi. What we’re waiting for is a sufficient recognition of the monetary disorder. You see monetary disorder manifested in super low interest rates, in the mispricing of credit broadly and you see it in the escalation of radical monetary nostrums that are floating out of the various central banks and established temples of thought...” - James Grant

Our economic view is not optimistic, but rather sanguine, and that in the archaic sense of bloody. We anticipate a recession in the US with about a ~60-70% probability starting sometime in the next 9 to 24 months. One colleague hopes for timing before the election so as to clarify the outcomes created by policy over the last decade or so. I think “Democrats hanging from the lamp posts...” was the phrase he used. Well, perhaps he can scratch that ambassadorship...

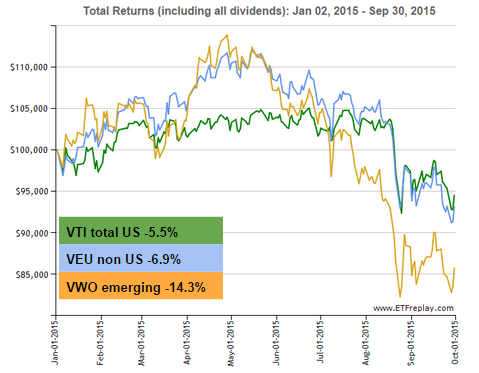

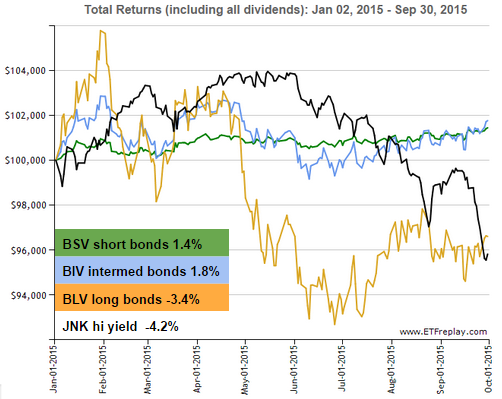

Returns of the broad equity and bond markets on a year to date total return basis

It’s not pretty. The US and developed foreign markets went negative in a large sell off related to earnings, China’s dismal economy, chaotic communication of policy by the Fed and grim geopolitical events. The emerging markets declined significantly with little current relief in sight.

The Fed

"I don't know why anybody believes the Fed's forecast. They didn't see the biggest recession in the postwar era coming." - Paul Kasriel, Chief Economist, Northern Trust Company, as in WSJ on February 13, 2012

A combination of chronic malinvestment (which means exactly what is sounds like) and excess leverage induced by defective tax, energy, regulatory, legal, and fiscal policies over the last near decade is the real problem. The Fed has directly enabled or aided & abetted much of it by extending monetary policy well beyond it's normal purview. QE & ZIRP have manipulated interest rates and thereby a host of asset values and risk appetites that depend on the general level of rates.

It is most easily observed in equities. Below we picture the Fed’s balance sheet with the S&P 500 and it speaks for itself. Note the “taper” as merely the sideways movement of the balance sheet.

Recall there has yet been no unwind, no real absolute reduction. We’re just going sideways and gotten a whiff of the equity response. But why?

“Interest rates... are universal prices: They discount future cash flows, calibrate risks and define investment hurdle rates. So interest rates are the traffic signals of a market based economy. Ordinarily, some are amber, some are red and some are green. But since 2008 they have mainly been green.” - James Grant

We see the same general impact of QE and ZIRP on Treasury rates and bond prices through the fixed income complex (rates down, bond prices up) essentially since 2009 with some interesting anomalies. The 10 year rate is the least controllable by the Fed, and notwithstanding Fed jawboning about raising rates, we see the 10 year actually declining since 2014. Perhaps the market isn’t buying the growth story?

Again how does this foster malinvestment? Again we’ll cite James Grant’s example from the oil patch:

"The central banks lifted off the stock market so that aggregate demand is going to rise. But they forgot to consider that aggregate supply is likely also to rise: Oil drillers will have it easier to find financing with which to drill the marginal well and to produce the marginal barrel of oil. This will weight on the market causing lower oil prices which will lead the central bankers in return to print still more money to save us from what they call "the risk of deflation." So it’s seemingly a never ending, circular process of so called stimulus leading to still more stimulus and unconventional ideas leading to radical ideas."

“All this monetary stimulus does two things in a reciprocal way: It pushes failure into the future and brings consumption into the present. Providing marginal businesses with very cheap credit is inviting companies that have passed their useful days [to] ... some kind of an afterlife thanks to the subsidies from the central banks...” (ibid)

Another easy example: it is this phenomena that will make for lower recovery rates on junk bonds in default; the final permanent losses to capital will be higher this cycle. Same with most everything in emerging markets. Manipulation always increases the amplitude of cycles because the Fed has tampered with the brakes. And this, in slightly less virulent form, is what we’re seeing in the equity and other markets and across the spectrum.

What the labor & credit markets tell us

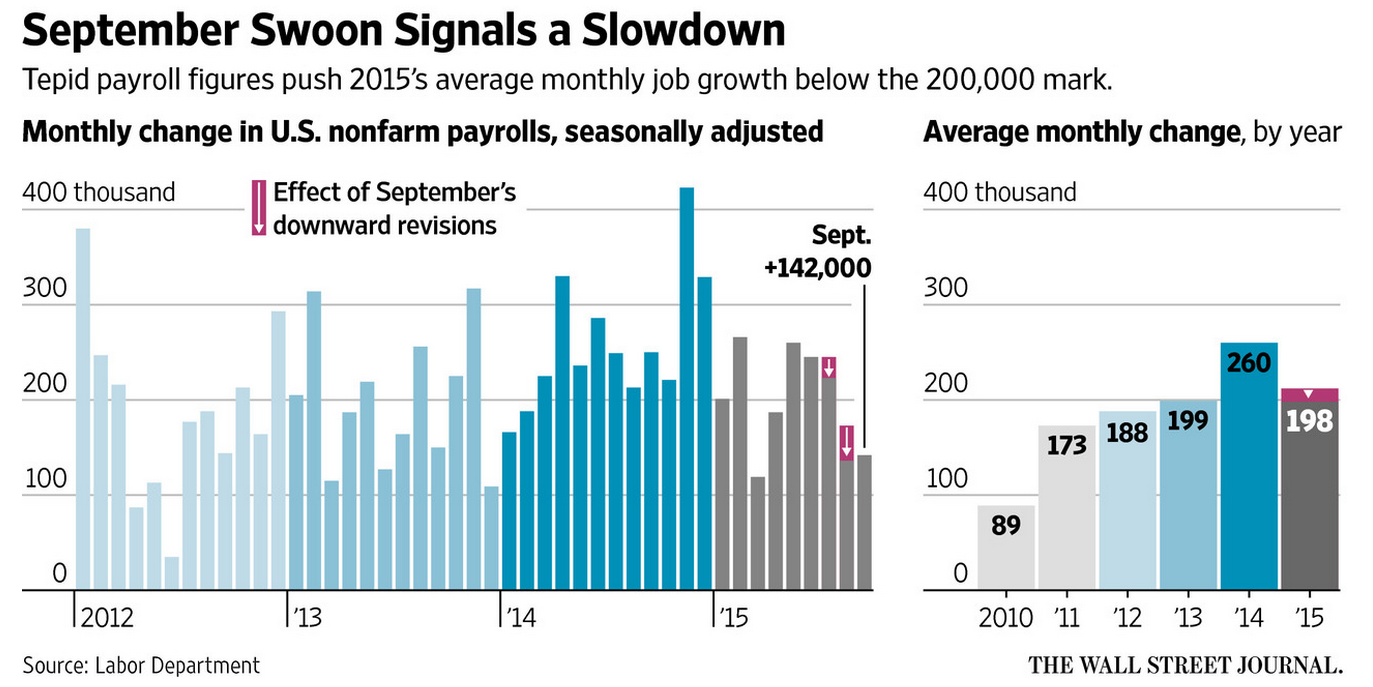

We look at the credit markets which have been tightening for some months now (indicated by rising spreads). We sense the Fed is late in the game. But why? Perhaps this little gem of Sept. 17 which went widely unnoticed gave them a pause: a -208,000 revision of the 12 month period ended March 2015 to Total Nonfarm Payrolls. “This is equivalent to eliminating nearly one full month of job gains in the specified 12 month period, and spread across the various months, would have meant a constant series of NFP headline misses instead of consensus beats...”

Add this to the recent and dismal September employment numbers and related revisions and the picture changes:

Typically the Fed tightens to slow down a booming economy, however, now it seems it is trying to raise rates into an already tightening credit market turn and a potentially weakening economy. It likely the Fed missed its chance to raise rates, if in fact there was a game called “recovery”.

Or even worse, perhaps the Fed is acting for the wrong reason. One suspects the Fed wants to raise rates because the Fed has created a monetary cul de sac and have finally realized they need to start unplugging Frankenstein.

Will this exacerbate the fragility of the markets, investor sentiment or volatility? Has it already? Look at the rising credit spreads where it seems July of 2014 was a significant turning point.

Fed late for high yield

Fed late for investment grade

Way late for commodities

Below is a dramatic price chart looking back 2 years for iShares S&P GSCI Commodity-Indexed (ETF ticker GSG) which is a broad index of commodity futures. Like the economy, it is heavily concentrated in energy, but nevertheless since January of 2014 it has declined ~48%. Not perhaps a sign of robust global demand?

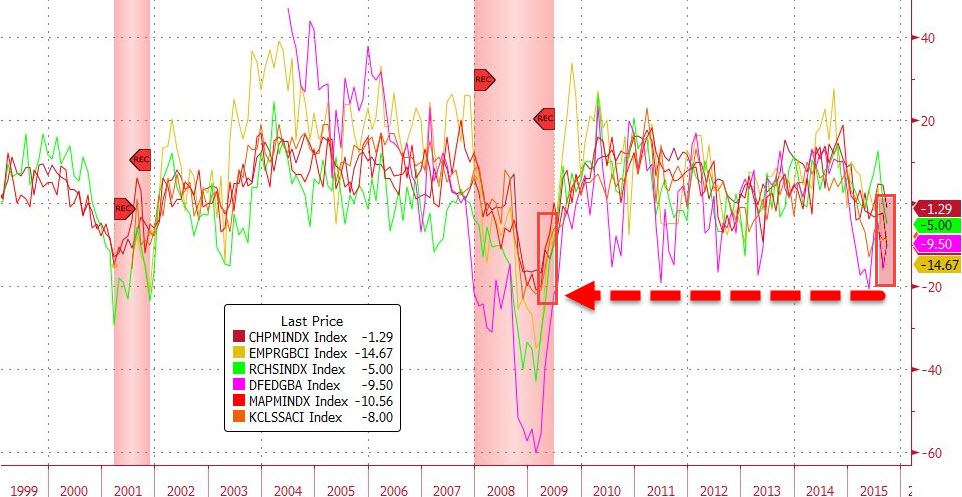

More troubling is that for the first time since 2009, all six major Fed regional economic activity surveys are in contraction territory.

source: graph from Bloomberg as in 6 Out Of 6 Fed Surveys Say US Is In Recession

We should point out that the Institute for Supply Chain Management’s (ISM) report on manufacturing released Oct. 10 shows modest growth in national manufacturing but with a declining rate of change, indicative of sideways to slightly positive growth. Nothing dramatic. The ISM report showed the Non Manufacturing Index of August at 59%, good results on an absolute basis, but a decline from 60.3% of July.

Consumer spending continues strongly, and we can’t figure out why.

What the equity markets tell us

We saw it in the first graph, but can it get worse? Yes. Will it? We don’t know, though we suspect it will. The equity markets reflect the same concerns that US Treasury rates do.

Our problem is not that our companies don’t know how to make & sell stuff that’s better, faster & cheaper to interested buyers. They actually do it quite well, best in the world. And for the most part they have robust cost structures & controls; excellent supply chains; solid balance sheets, and decent & continuously improving governance structures. Many of the obstacles facing our economy are non-monetary in nature and have grown substantially.

But harken back to the disruption of the price mechanism & related feedback. If you’re pricing a financial instrument and are uncertain as to what the market determined rate is relative to the synthetic one of the Fed, you’re not really sure whether you should buy or sell. Is the price good? It depends... The same fog covers broad investment and hiring decisions in the real economy: do we build a new plant & hire? It depends...

Meanwhile all are looking at the “monetary moment” and don’t know which way the pendulum will swing. Uncertainty creates volatility, and volatility impacts investor behavior. Mohamed El-Erian in today’s Financial Times looks at the structural issues:

“When thinking about the consequences of such a regime shift, it is tempting to segment the investor universe into three: “fast money” that sees higher volatility as enhancing trading opportunities; volatility driven strategies, such as value-at-risk and risk parity strategies that are vulnerable to disorderly deleveraging; and long-term institutional funds, whose first inclination is to treat volatility bouts as noise rather than consequential events that affect their investing behaviour in any lasting manner.

Given the degree to which the third pool of money dominates the first two in size, and to the extent that it tends to rebalance on a periodic basis (by shifting more assets into core equity holdings whose prices have declined sharply relative to bonds), this characterisation is an inherently reassuring one. It suggests that damage from higher volatility should prove temporary, contained and reversible. But it may also be misleading for this particular moment in markets.

While the counter-cyclical rebalancing of institutional investors is stabilising, it does not “stick” if a structural shift in volatility causes a more generalised reduction in risk exposures. Specifically, a significant and durable shift (which I believe this is) affects the methodology that anchors the “neutral” asset allocations of many institutions (also known as their policy portfolios). It is only a matter of time until this new volatility paradigm lowers the average risk levels of neutral asset allocations.”

That’s pretty ethereal fancy-speak. We think he has cause and effect confused. It’s not the volatility that will cause a synchronized derisking, it is the absence of growth and the overleveraged state of global finances. Distressed companies display the same phenomena: one watches the top & bottom lines slow while the debt compounds. It forces decisions.

So, if you’re the Fed in the laboratory and trying to unplug Frankenstein before he gets off the table, you’re not too concerned with anything else. And the peasants with pitchforks & torches are gathering at the gate. But hey, Ben, sometimes there just aren’t any good solutions, you know?

We still like short term investment grade fixed income product, however, more and more we are contemplating extending duration a bit, but the call is difficult, one we’re not yet ready to make. The Fed has lost what little control it had over the long end, and if our economic view is correct,the rate hike is in the cooler for a while.

Equities will be sideways and volatile. Further declines may provide new values for rebalancing and some may be substantial, but absent growth the timeframe for recovery of value could be prolonged. We do hear Mr. El-Erian's comments, and our sense is that many investors, individual and institutional alike, are carrying more equity or other risk than they can tolerate, either emotionally, financially or from a regulatory perspective. This will add volatility, but we must remember the real drivers of our economy are profits & efficiency. Watch for top line growth of corporate America. It is a necessary indicator of real recovery, and it may be a while in coming.

"The curious task of economics is to demonstrate to men how little they really know about what they imagine they can design.” - FA Hayek

hb

hb

Reader Comments