Fed: now go do that voodoo that you do so well

The great Unwind of the Fed has now arrived, and we are grateful for it’s modest and seemingly benign form:

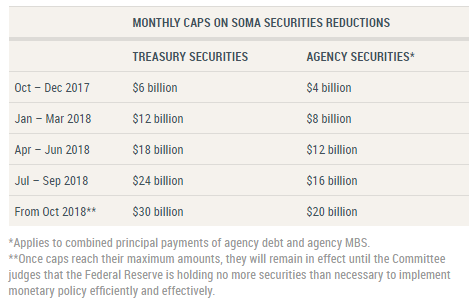

the Federal Open Market Committee directed the Open Market Trading Desk at the Federal Reserve Bank of New York to initiate, in October 2017, the program to gradually reduce the reinvestment of principal payments from the Federal Reserve’s securities holdings that is described in the Committee’s June 2017 addendum to its Policy Normalization Principles and Plans. Specifically, the Committee directed the Desk to reinvest each month’s principal payments from Treasury securities, agency debt, and agency mortgage-backed securities (MBS) only to the extent that such payments exceed gradually rising caps.

The schedule of monthly caps consistent with the Committee’s September 20 decision and the June 2017 addendum is as follows:

So, at least for the very short term we know what they are doing, at least until that may or may not change. We confess to a severe limitation as to cyphering what the unwind means in respect of the global markets and our portfolios. We are reduced to mere astragalomancy and suspect we are in large company, including the Fed, policy mugwumps, along with most institutional & retail investors, and captains of industry, though few can so admit. No one knows because the system is too complex and dynamic.

As background, quantitative easing was intended to 1) soften the blow by extending the time horizon over which huge financial losses were realized and 2) accelerate broad economic growth after the Great Unpleasantness. It was interwoven with other policies which included the manipulation (or one might more charitably say “management”) of interest rates by central banks and the transformation of risks of financial institutions to sovereign risk.

The problem, however, is that the growth never showed up. The nominal values of financial assets skyrocketed. Central bank strategies were generally globally coordinated and synchronized.

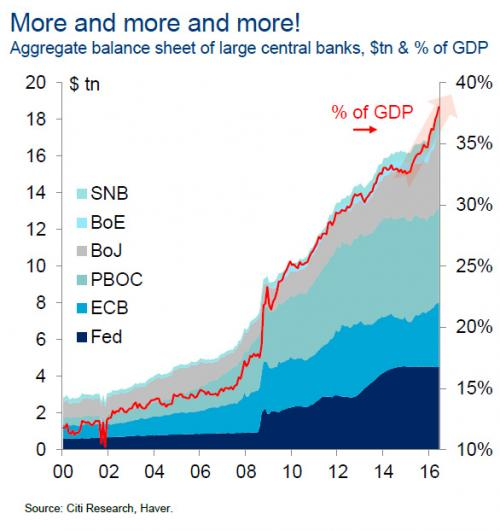

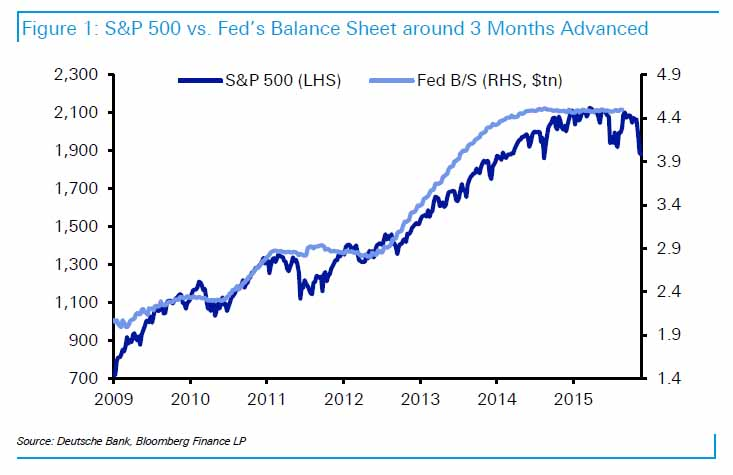

Central bank balance sheets exploded

Source: http://www.zerohedge.com/news/2017-05-06/problem-emerges-central-banks-injected-1-trillion-2017-its-not-enough See also: Yardini: https://www.yardeni.com/pub/peacockfedecbassets.pdf

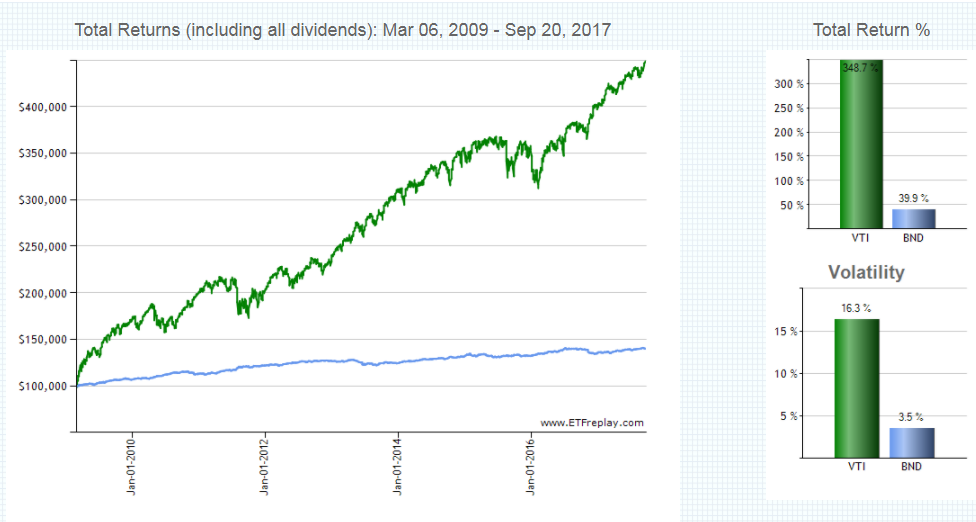

Financial assets took a ride on the rocket

Since the low of March 6, 2009, the US market is up ~350% or 19.2% as an annual compound rate on a total return basis (below the total returns of Vanguard Total US Stock Market, VTI). If you were in the market, you were getting returns of leveraged equity stubs (LBO’s). Well, you were... kind of.

Source: www.ETFreeplay.com

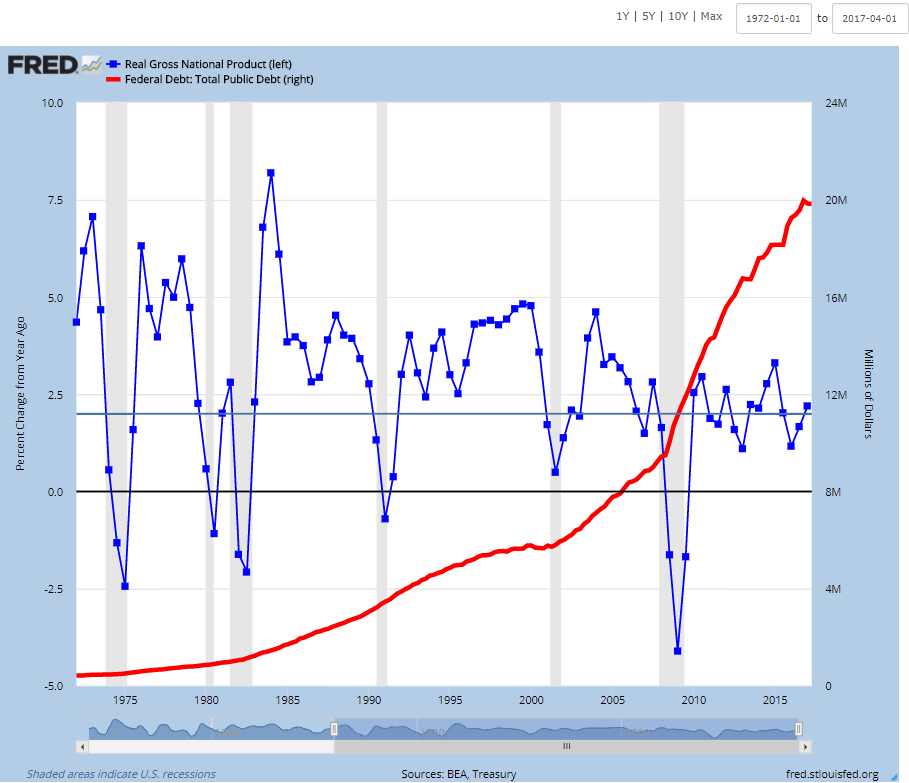

But economic growth has been weak

Now, let’s look at real GDP growth: anemic. The blue/greyish horizontal line in the graph below is set at 2% for reference. We threw in the Federal debt just for fun: check where it was in 1972.

If you want further information on growth of real median personal, family and household incomes look at the charts here. No one is throwing a party.

So what’s driving the financial markets?

Well, it’s not robust economic growth. Let’s combine the pictures of central bank balance sheets and the market:

Do we see a pattern? Yes, but is it cause & effect or association? We suspect partially or mostly causal. To some degree investors were forced into risk assets in face of low or negative nominal & real rates in the fixed income markets. The funds started to flow but the transmission mechanic to the real economy was broken. Consider the perspective of an investor faced with uncertainty of the economic and regulatory fundament, not to mention all kinds of disruptive technologies. Let’s see, shall we make long term investments in capital expenditures (new plants, systems, employees, etc.) that may take 5-7 years to develop or buy financial assets that can be divested with a click? One also might consider whether politicians and the regulations they write may be cheaper & easier to buy & sell than capital goods.

And now we wonder along with Fitch:

"Looking ahead in the rating cycle, the most benign credit market conditions in modern history will gradually begin to normalise as central bank assistance is withdrawn and world growth peaks in 2018...Unwinding QE will pose challenges to both borrowers and lenders, including the many sovereigns with post-2000 high government debt-to-GDP levels. With a number of markets appearing to be approaching cyclical peaks, it may also expose potential asset bubbles...”

https://www.fitchratings.com/site/pr/1029367

Policy uncertainty

The “Trump trade” seems to roll on, at least in the equity markets, and we have no idea as to why. Effective tax & health care reform are hugely important to future growth, but we don’t see either as highly probable. We do see progress on energy policy. It’s hard not to conclude that Congress is dysfunctional. Moreover, there is no hope for a weight of consensus that gives allocators of capital any confidence in the duration of any political policies or regulations that impact long term investments. Why invest if the mode today may be reversed tomorrow?

More troubling to us, however, is that no one is talking about our most important issue, the debt crisis - to include funded and unfunded pension and social liabilities - that is upon us. Leveraged entities have less flexibility to invest and grow... or to accommodate unforeseen contingencies. They tend to go bankrupt or be sold to competitors, and nations, states and municipalities are no different, except that the “liquidation sale” for these entities takes different forms, including a declining standard of living, loss of social order, and frequently geopolitical subordination. One inspects the edges of cloth to find the frays, yes?

Much uncertainty traces to our ‘data dependent’ Fed policy. Might we be so bold to suggest there is one minor data point they seemed to have missed? The world seems a bit more fragile these days... and so seems because it is.

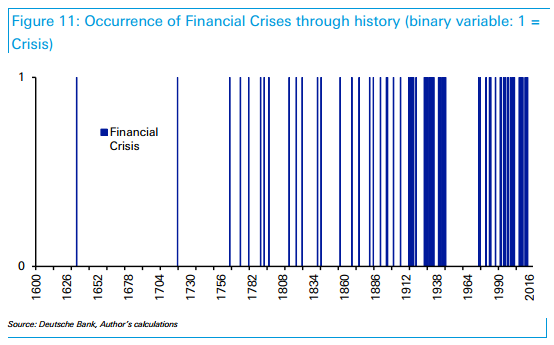

Source of graph and quote: Deutsche Bank, Long Term Asset Return Study, The Next Financial Crisis, Sept 18, 2017

See a pattern of increasing frequency of stress since the Bretton Woods system collapsed in early ‘70s? “Interestingly [the] period between the mid-1940s and early 1970s was the longest stretch without an observable financial crisis for 200-300 years.” We observe where money meets fiat currencies, central banking, moral hazard, and leverage.

Equity valuations are high by most benchmarks, more so by others.

S&P 500 PE ratio

Shiller PE ratio

Price to book ratio

Source for valuation ratios: http://www.multpl.com/

Fixed income

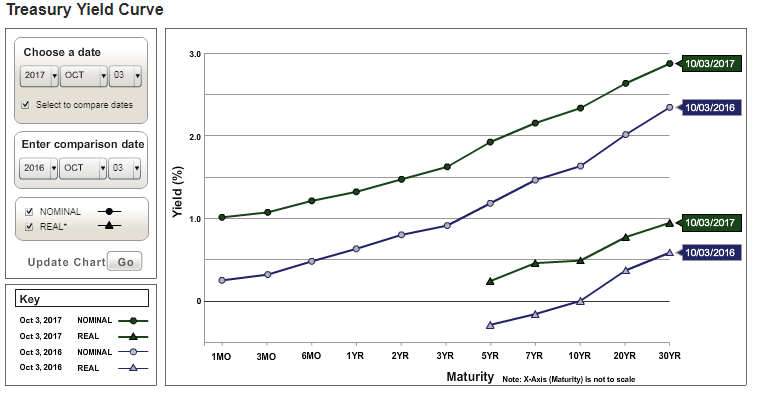

Nominal and real rates have risen relative to a year ago. Today an investor can get slightly less than a 1% real yield (~ 2.9% nominal) on a 30 year bond. It’s an improvement over near zero. Well, we have to start somewhere...

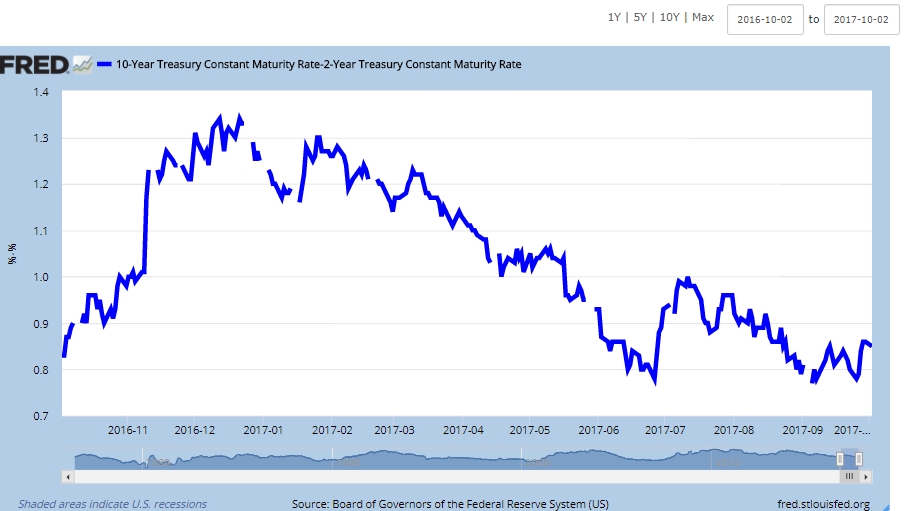

The yield curve continues to want to flatten, although we note the recent uptick, no doubt driven by anticipation of the Fed’s change of balance sheet policy. A flattening yield curve is generally a weak sign for the economy.

Inflation expectations of the markets seem stable although slightly below target ~ 2%

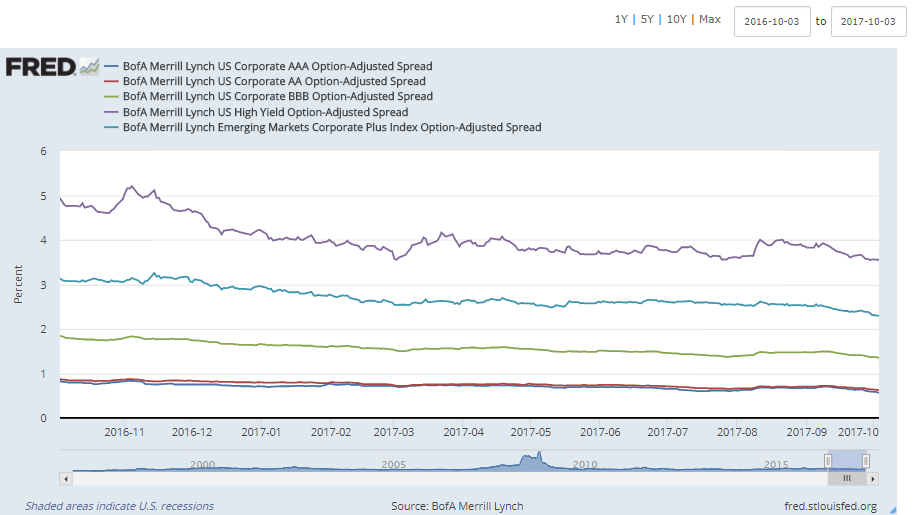

Credit spreads: stable, steadily declining

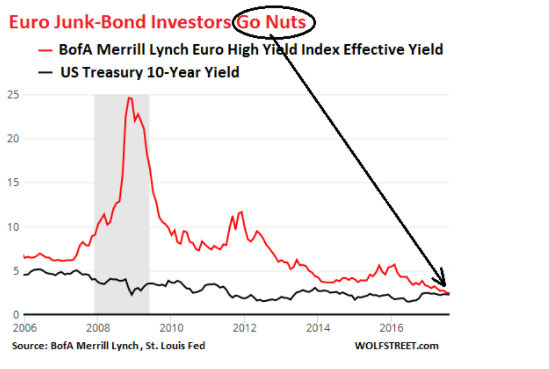

But the real fun is in Euroland: a bit bubbly yet?

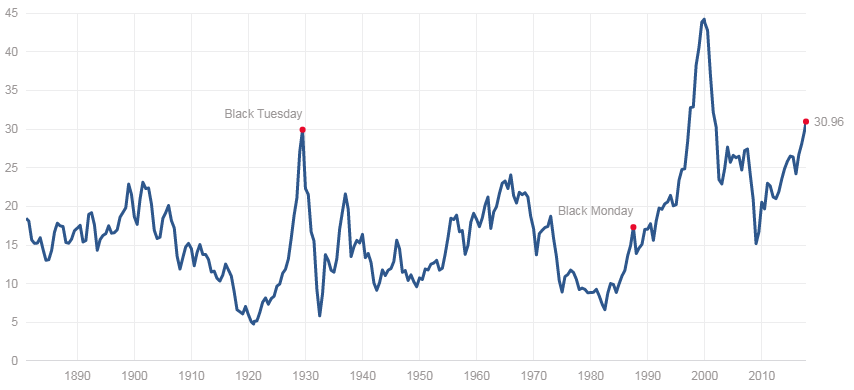

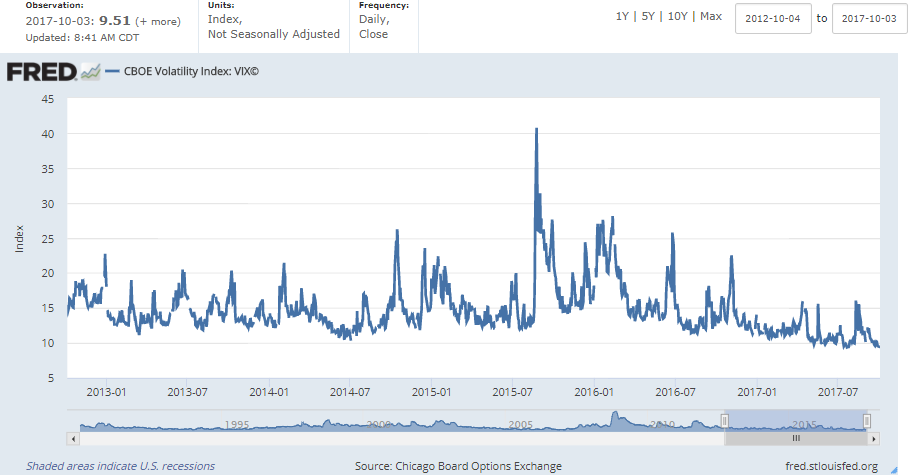

Look ma, no vol!

The volatility of the equity market is near all time lows. One supposes someone must have faith, however, we do not believe VIX is an indicator of either market risk or investor sentiment. We believe the signal of volatility (or its absence) can have significantly different, if not opposite, meanings in different contexts. Regardless of our view measured volatility of the equity market is at record lows, and we don’t get it.

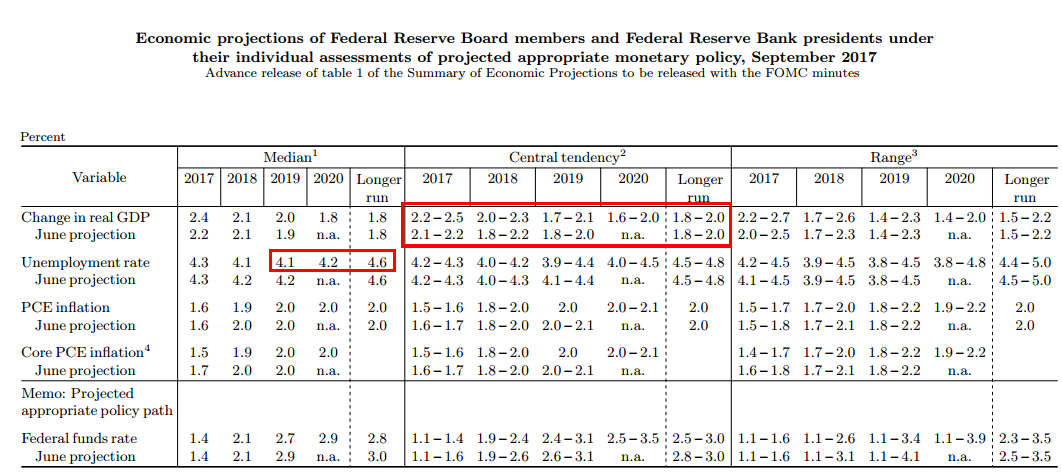

Expectations of future growth: not robust from the Fed

Source: Fed release Sept 20, 2017

What to do?

Uncertainty demands diversification. We hew closely to our asset allocations which generally tend to mirror the global efficient portfolio, with risk primarily managed by equity and duration constraints. We tend to be sector neutral, meaning that we tend towards market cap weightings, in both equities and fixed income.

This discipline has for the most part resulted in serially selling off equity gains over time and re-allocating to fixed income. Call us primative, but we like the notion of selling high and buying low in long term and risk constrained context. It’s not glamorous.

We still hold a favorable view of short term investment grade product in fixed income, but are considering a more normal or traditional structure of duration. We have been for some time. Maybe the unwind of QE can be a catalyst of normalcy after some dust settles... and we hope it’s just dust. There may be some take back of that long series of equity gains if things don’t go well.

Stuck in the mud

Our national problem with debt and unfunded liabilities continues to compound, and we lack the political framework and will to resolve them. As to policy and economic uncertainty, well, nothing has changed. As we’v said in our blog some time ago, this is how we lose decades:

All are plagued by uncertainty which freezes the status quo leaving inherently destructive processes that aggravate or allow the legacy problems to compound without limit. It is a failure of government. Or rather a government of failure. Congress & the Administration impair investment, liquidity & employment and increase systemic risk… essentially guaranteeing continued low growth while the problems worsen.

This is not genius at work. - A Little More Perspective , June 25, 2013

And Europe?

Europe’s economy is in no better state today than it was in 2009. It is, in fact, worse off today than at the official trough. The contraction has not ended, it has only become more misunderstood and complex.

http://www.alhambrapartners.com/2017/09/25/distinct-lack-of-good-faith/

The big picture is bigger than the markets.

The real danger of 2016 and immediately beyond, then, is this race; those that are catching up to the real problem and trying to find a real solution not of inflation or deflation but of stable money will need time to find and then implement it (this is where the lost opportunity of 2008 is so tragic)... But as confidence in the old order falls and the strong populist desire to look elsewhere begins to take its place, into that messy void is still the potentially disruptive force of bad economics. Where do all these curves meet? In other words, what is the point at which shrinking faith, desperate central banks, and growing economic despair all conspire to push us into the darker reaches?

Unfortunately, we are likely much closer to the edge than anyone would readily admit. After nearly a decade of stagnation and attrition, the forces of stability are already worn thin. That is the essence of the populist revolt, a response to years and years of getting nowhere. What has changed in the past few, especially under this "rising dollar" or dollar shortage, is that the populists have been proven right; following further down the mainstream path has led nowhere but to more uncertainty and greater anguish. Time is now the biggest cost. -Jeffrey Snider, Alhambra Investments in

It’s not all about investments. As Larry Kudlow says, “Keep the faith.”

hb

hb

Reader Comments